Shipbuilding and repair

- Details

- Category: Construcción Naval

- Published on Wednesday, 18 March 2026 22:17

- Written by Administrator2

- Hits: 229

https://op.europa.eu/webpub/mare/eu-blue-economy-report-2025/

The fleet flagged under EU Member States accounts for approximately 12% of the global fleet, with 15 096 vessels registered as of the second quarter of 2024. In terms of gross tonnage (GT), the EU fleet constitutes over 14% of the global fleet, amounting to 236.3 million GT, while it represents approximately 13% in terms of deadweight, totalling 298.8 million tonnes.

As of the second quarter of 2024, the fleet registered under EU Member States includes a diverse range of vessel types, both in absolute numbers and percentage. It accounts for nearly 27% of the global RoPax fleet (transport of passengers and vehicles, 912 ships), almost 23% of the world's passenger vessels (1 226) and more than 18% of the global containership fleet. In absolute terms, the most prevalent ship type was fishing vessels (2 540), followed by tugs/dredgers (2 007) and general cargo ships (1 468).

The EU's shipbuilding industry comprises approximately 150 major shipyards engaged in the construction of various types of vessels, both civilian and naval, as well as platforms and other maritime equipment. According to the European Maritime Safety Agency, in 2023, around one in eleven ships was built in an EU shipyard, with the majority consisting of tugs/dredgers (38), fishing vessels (29), general cargo ships (29), and passenger ships (26).

Average age of ships varies notably by the type, with FPSOs (Floating Production, Storage, and Offloading units), passenger ships and refrigerated cargo recording more than 30 years (33.2, 30.5 and 30.1, respectively).

At the opposite end, chemical tankers, containerships, bulk carriers and liquefied gas tankers have been built on average less than 15 years ago (14.1, 13.4, 12.4 and 10, respectively). Age is intrinsically related to end of life. In 2023, a total of 437 ships were recycled worldwide. Among them, 22 were dismantled at EU ship recycling facilities, while four EU-flagged vessels were scrapped outside the EU.

Shipbuilding and repair includes the following sub-sectors:

- Shipbuilding: building of ships and floating structures; building of pleasure and sporting boats; repair and maintenance of ships and boats.

- Equipment and machinery: manufacture of cordage, rope, twine and netting; manufacture of textiles other than apparel; manufacture of sport goods; manufacture of engines and turbines (except aircraft), and manufacture of instruments for measuring, testing and navigation.

Size of the EU Shipbuilding and repair sector

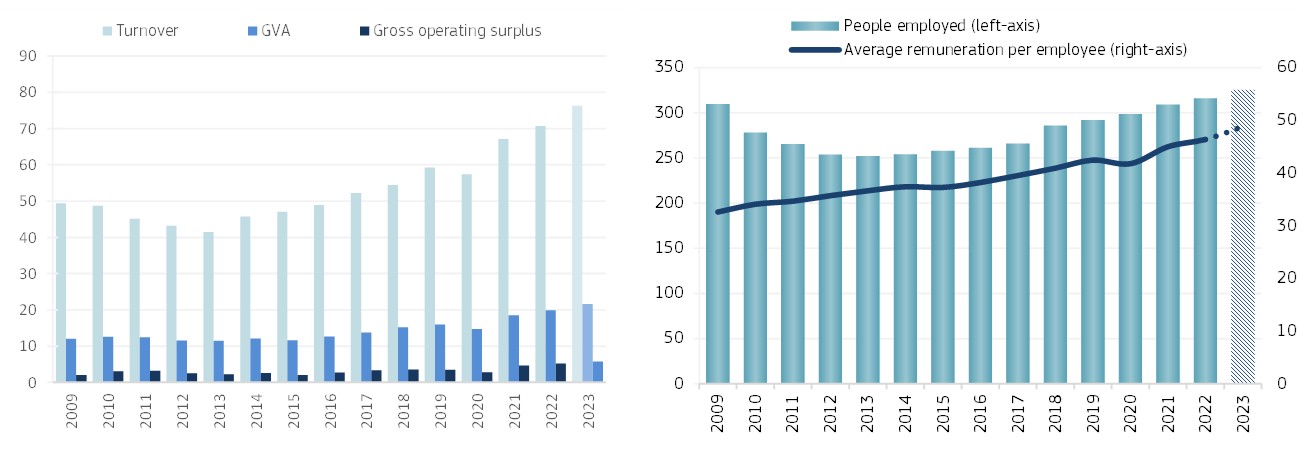

The sector generated a GVA of EUR 19.9 billion in 2022, a 7% increase compared to 2021. Gross profit, at EUR 5.2 billion increased by 14% on the previous year. The turnover reported for 2022 was EUR 70.7 billion, recording a 5% increase on the previous year (Figure 1).

In 2022, about 316 000 persons were directly employed in the sector (2% increase on 2021), and the annual average wage was estimated at EUR 46 400, up 3% compared to 2021.

Estimates for 2023 indicate an increase in GVA, gross profit and turnover between 8-10%. Also, an increase in persons employed and average remuneration is estimated between 3-5%.

The European shipbuilding industry [1] experienced a surge in 2023, with a total of 101 new orders being placed at European shipyards. This represents a 9% increase over the previous year, driven primarily by a surge in demand for dry cargo vessels, which accounted for 71 of the new orders, as well as cruise ships, with 11 new orders recorded. This growth is second to the Chinese orders (+29% on a year-to-year basis), which confirms its position as the top shipbuilding nation globally. Indeed, China recorded a market share for new orders of 63.2% (+11.7% from previous year), whilst European market share increased very marginally to 5.6% (from 5.4%).

[1]The figures are based on the BRS Group, 2024 – Shipping and Shipbuilding Markets – Annual Review 2024 edition. The European market under examination includes the following countries listed by decreasing number of cumulative orders on the book: Italy, France, Germany, Finland, Turkey, the Netherlands, Poland, Croatia, Spain, Romania, Azerbaijan, Portugal, Ukraine, UK, Greece and Norway.